The Telecom Operators VBE model - Part 2

Part 2 covers the Challengers to the traditional telecom equipment manufacturers VBE model and the different technologies they are trying to bring into communications. Communication has been a basic human need and since times 10000 years ago humans have had communication and the forms of communication have changed over the years. We look at the new technologies trying to gain a foothold in this area dominated by traditional players.

Abhijeet Kelkar

3/31/20255 min read

This series examines the VBE model in telecom. In Part 1, I explained why telecom equipment companies struggled with 5G sales and how my VBE analysis predicted this five years earlier. The prediction was based on three key questions to stakeholders—telecom operators, their revenue models, and cost and value to end users. In this second Part we look at the challengers to the company’s existing VBE model around data and data monetisation.

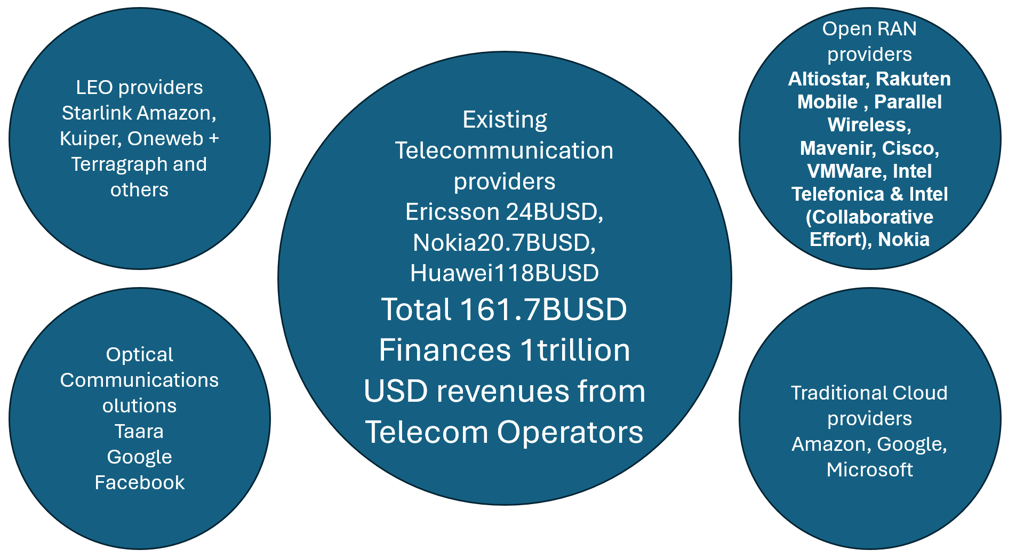

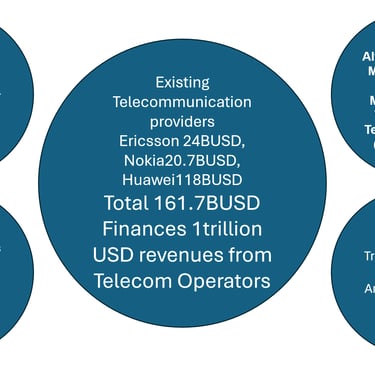

Now, history is repeating as new challenges emerge for telecom equipment providers. In this part, we explore rising competitors like LEO satellite companies (e.g., Starlink), optical communication (e.g., Taara), and data giants like Google entering the telecom space. And the emergence of Open radio access network (Open RAN) as another factor.

Open RAN is gaining popularity in telecom due to its interoperability, flexibility, and cost savings over traditional proprietary RAN systems. Here is why it is trending:

1. Breaking Vendor Lock-In

Traditional RANs require hardware and software from a single vendor (e.g., Ericsson, Nokia, Huawei), while Open RAN allows operators to mix components from multiple suppliers, reducing vendor dependency.

2. Cost Reduction

Open RAN cuts costs by using off-the-shelf hardware and open-source software, reducing both capital and operational expenses.

3. Innovation & Flexibility

Open RAN enables telecom companies to customize networks and integrate recent technologies quickly, optimizing network performance with AI and cloud solutions.

4. Support from Governments & Big Tech

Governments, especially in the US, UK, and India, support Open RAN to reduce reliance on Chinese vendors like Huawei. Tech giants like Rakuten, Meta, Google, and Microsoft are investing in Open RAN innovation.

5. Enabling 5G & Future Networks

Open RAN supports 5G expansion, particularly in rural areas, and lays the groundwork for 6G, where AI-driven, software-based networks will dominate.

Challenges to Open RAN Adoption

Performance concerns: Open RAN networks may initially have higher latency than proprietary RAN.

Interoperability issues: Different vendors' equipment must work seamlessly, requiring standardization.

Resistance from incumbents: Major vendors (Ericsson, Nokia) have been reluctant to fully embrace Open RAN as it threatens their business model. Some Open RAN vendors are Altiostar, Rakuten Mobile, Parallel Wireless, Mavenir, Cisco, VMWare, Intel Telefonica & Intel (Collaborative Effort), Nokia (Open RAN commitment). While traditionally a closed RAN vendor, Nokia is embracing Open RAN and has committed to developing Open RAN solutions alongside its traditional offerings. Amdocs

So, the figure below illustrates the challengers to the existing Telecom Suppliers VBE model.

In this part, I see a repeat of history as the factors that affect sales of the telecommunication equipment providers piles up for a second accident.

In this part we look at the challengers to the existing Telecom companies VBE model. In the part 1 we looked at LEO satellite companies like Starlink from Elon Musk and Optical communication solutions like Taara and data companies like Google are trying to come into the telecommunications equipment area.

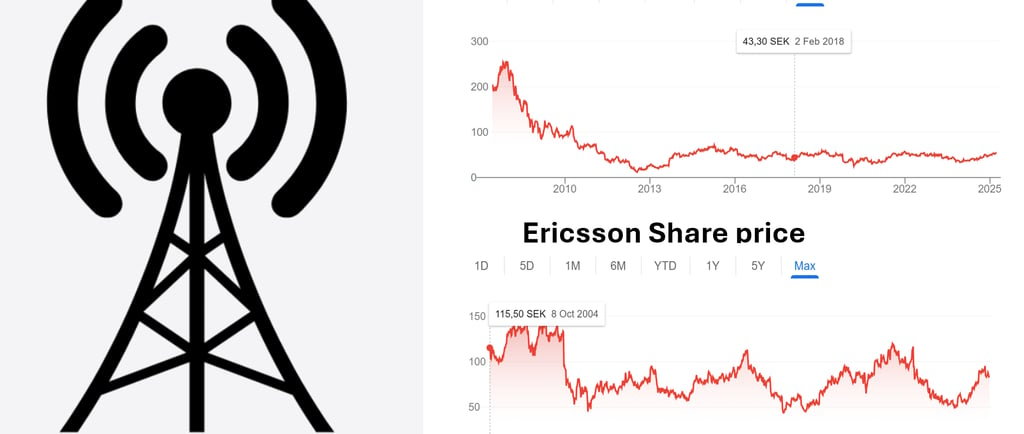

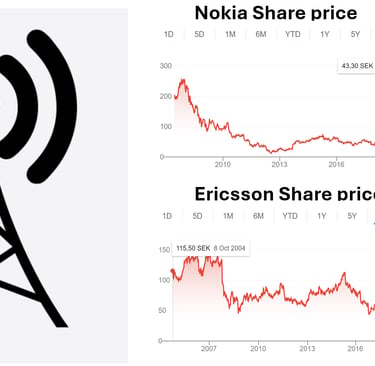

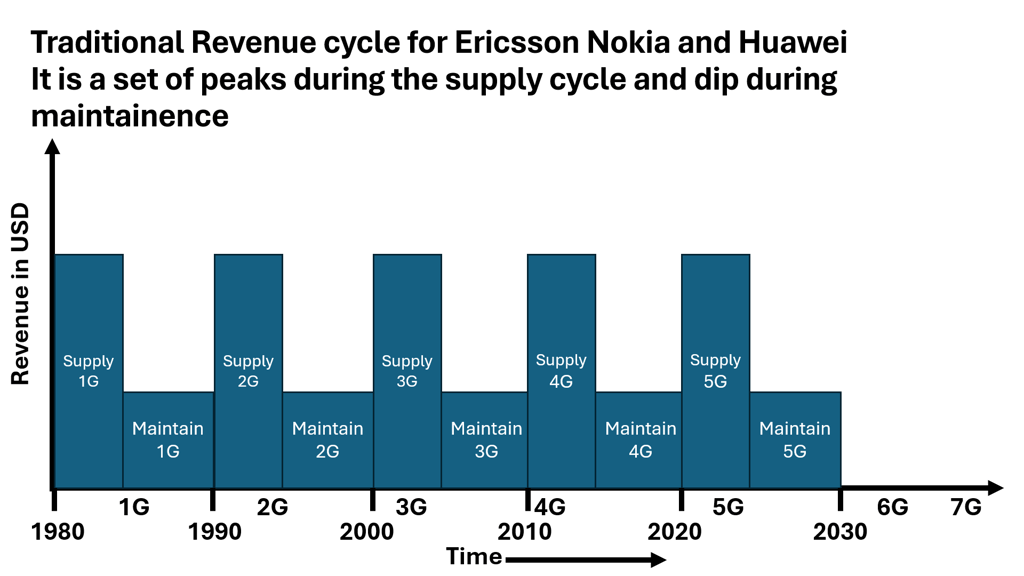

What we see from the diagram below is that the existing players Ericsson Nokia and Huawei work on a traditional supply and maintain model where the revenue is good during the supply part and dips during the maintain part.

This is how the demand works from the telecom operators side, a peak during purchasing new equipment and a dip during the maintenance phase for the new equipment.

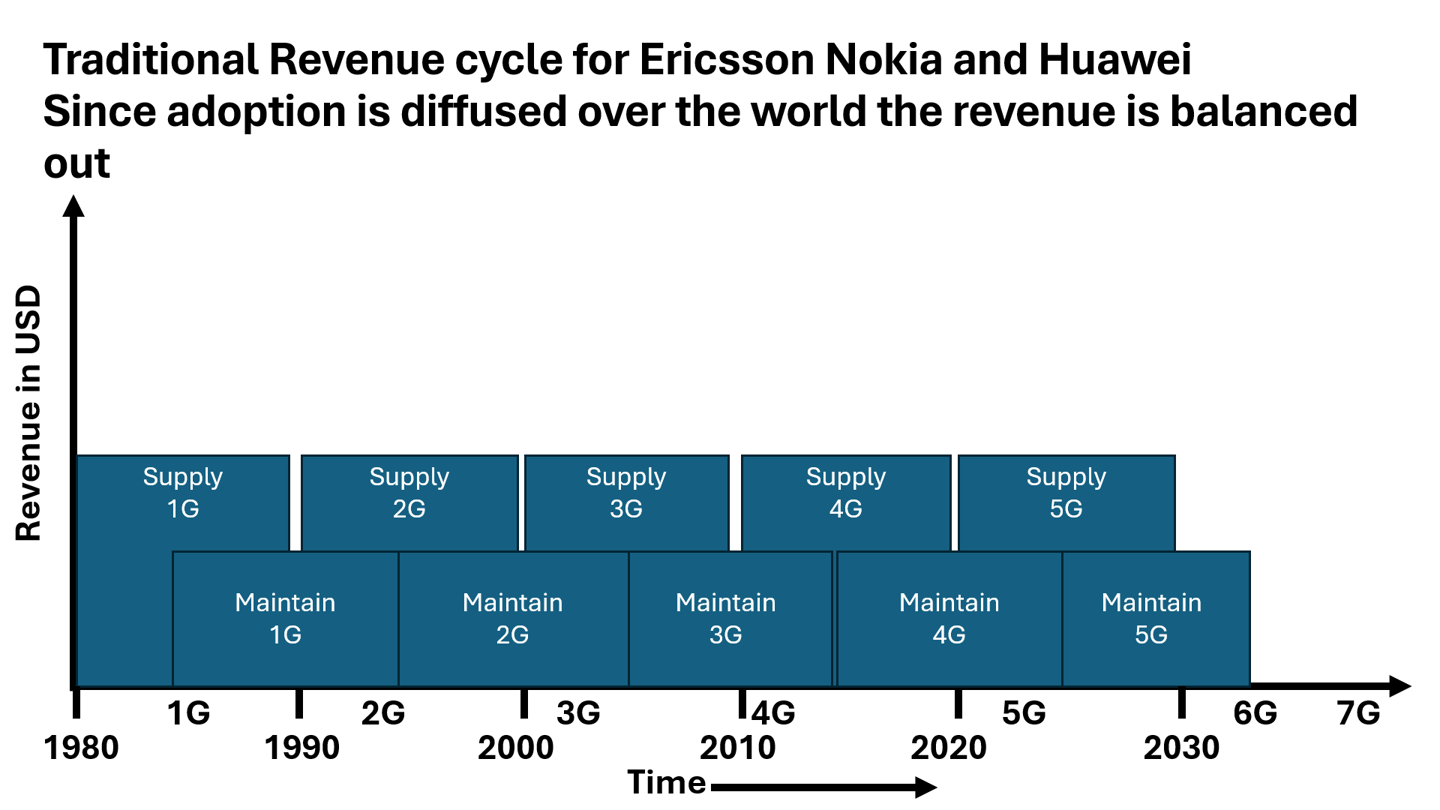

As all operators buy equipment over time the revenue is diffused and stable.

The revenue model is based on a high revenue equipment sales followed by a low value maintainence phase

However, across the world the telecom operators do not buy immediately after the introduction of new generation equipment hence we get a diffusion in the buy pattern globally which is reflected in the Ericsson revenue being stable over the years as per diagram below. But what is interesting to note is that their revenues will dip during maintenance phase and be up during the supply phase.

And this has resulted in Ericsson, Nokia, and Huawei, more interested in the supply of next generation equipment to keep revenues growing, while the telecom operators are going in the direction of keeping capital expenditure low and recover money from providing connectivity services to their customers. Hence, they want open RAN networks where they can buy off the shelf equipment and upgrade and maintain their infrastructure costs to a minimum. The VBE model direction is also looking at solutions where infrastructure for communications would cost minimal and at solutions where the payments could be in Data like the google or Facebook model.

In the Facebook or Google freemium model, the search or friends service is free but the payment for maintaining the infrastructure for maintaining these free services comes from the user’s data. Now here is where there will be a double whammy for the likes of Ericsson, Nokia, and Huawei if they fail to innovate their VBE model.

Face book and Google have already proven that the infrastructure required for communication can be paid for with the data of users which is monetised by them using the advertising model. And here is the kicker, The telecom operators are sitting on some very lucrative positions which the Equipment makers can help monetise.

So, the next part will cover the pieces of real estate the telecom operators sit on but go about with a begging bowl as they are unwilling to work on their VBE models.

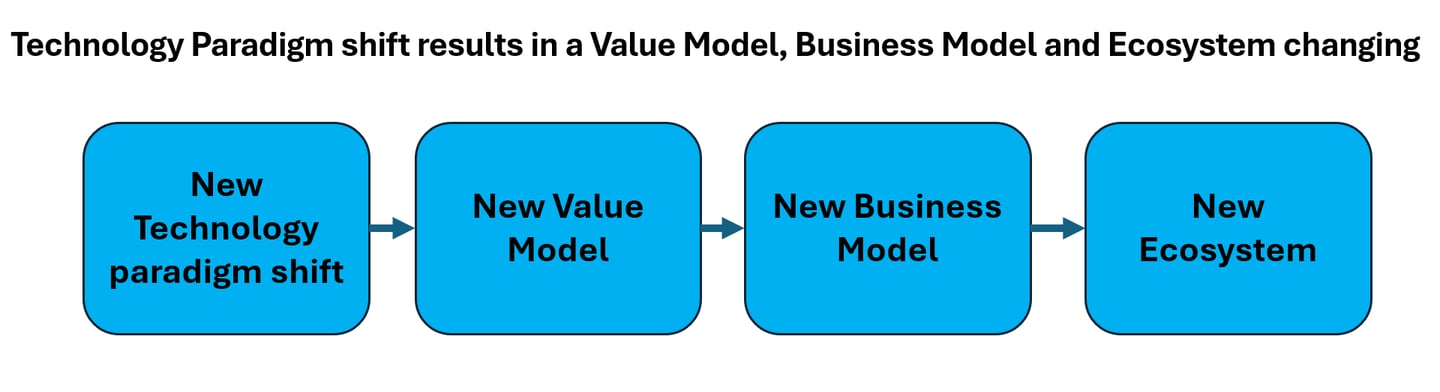

One more crucial factor about VBE models to consider is the change any Technology has on the VBE model, and this has been explained in the VBE model explanation video. And that factor that has played out for the last 200 years is the change any new and better technology can bring to the existing VBE model and given the different competitors challenging the existing VBE model of Ericsson, Nokia and Huawei, it is only a matter of time before the competitors tie together a model around the unconnected segments for communication. And that dynamic is explained in the diagram below.

Every new technology pardigm shift leads to a new VBE model.

In the next part we examine why the Telecom equipment companies like Ericsson, Nokia and Huawei need to change their operating model from a data pipe operator equipment supplier model to an Identity and Data enabler supplier model. And why they should use the existing imprints they are already sitting on to their advantage in the new VBE model.

Insights

Transforming business analysis for future resilience.

Consulting

Strategy

info@geoown.com

© 2025. All rights reserved.